Recent legal rulings surrounding bail hearings and immigration policy have reignited focus on the procedural limitations regarding the detention of immigrants without a bail hearing. For investors with an eye on legal services stocks, this development serves as a unique catalyst that could reshape demand for immigration representation, litigation support, and court services. This article explores how these changes may influence stock valuations in the legal services sector, spotlighting three companies that could benefit from this ruling. The aim is to assist you in evaluating whether these legal stocks merit closer scrutiny.

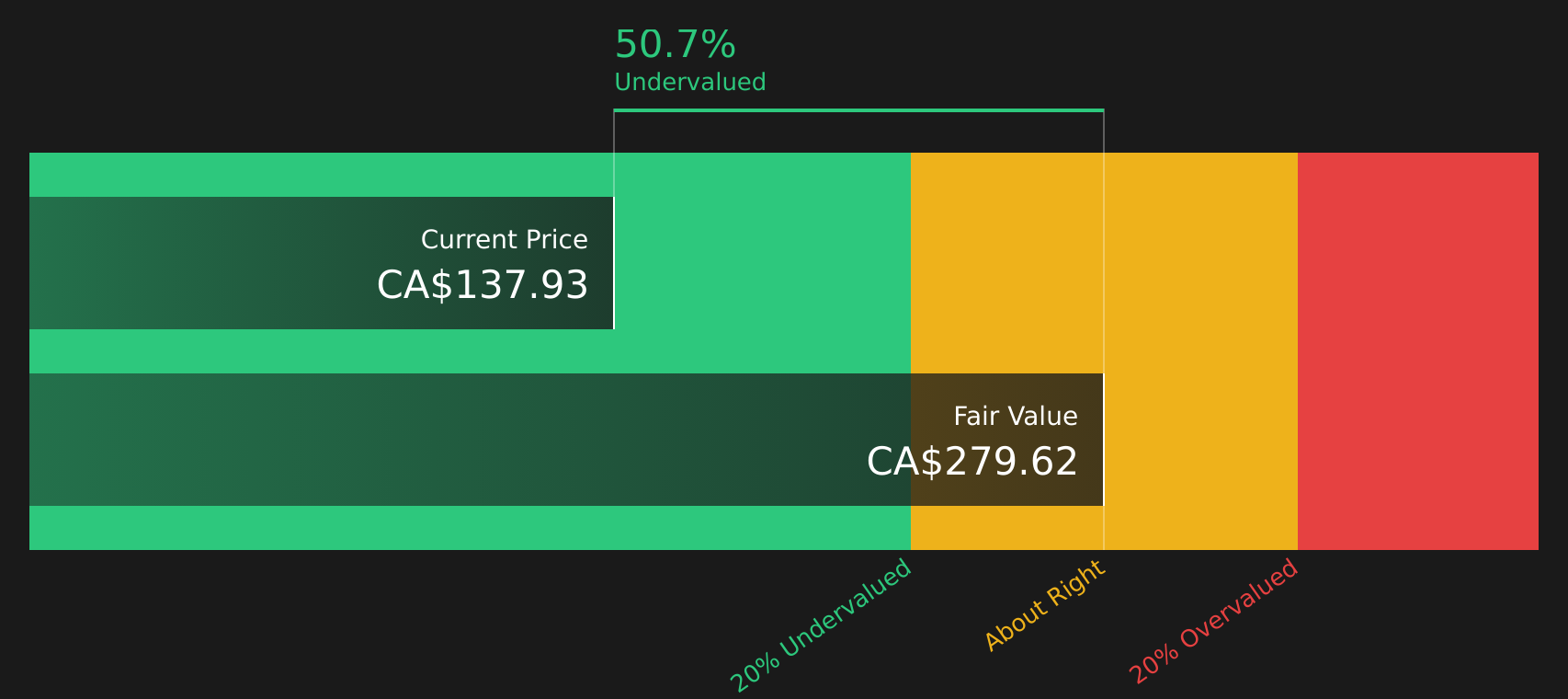

Robert Half

Company Overview: Robert Half specializes in professional staffing and consulting, connecting businesses with both contract and permanent talent across various sectors, including finance, technology, legal, and management. Its Protiviti division further enhances its offerings with business consulting services.

Financial Performance: The majority of Robert Half’s revenue, approximately $3.4 billion, is derived from its Contract Talent Solutions, followed by Protiviti Consulting at around $1.9 billion and Permanent Placement Talent Solutions at about $436 million. Minor intersegment eliminations total approximately $484 million.

Market Capitalization: USD 3.4 billion.

Positioning: Robert Half finds itself at the nexus of stricter immigration oversight and heightened court demands. The Protiviti division supplies specialized legal and administrative staff to manage bond hearings alongside providing compliance and risk advisory services for government and commercial clients. Despite analysts projecting earnings growth from a currently low-margin base, concerns about execution risks linger, highlighted by a recurring margin of only 2.4% and modest revenues, including a net income of USD 13.79 million in Q1 2026. While the stock’s dividend yield of 7.05% attracts attention, the combination of coverage concerns and potential risks tied to increased financial obligations necessitates cautious evaluation by investors looking to position Robert Half within their legal services portfolio.

Robert Half’s attractive 7.05% dividend yield, combined with its thin margin of 2.4%, raises significant questions about market perceptions, particularly in relation to the company’s discounted cash flow (DCF) valuation.

Thomson Reuters

Company Background: Thomson Reuters is a global leader in content and technology, delivering essential research tools, workflow software, and news services to legal, tax, accounting, and corporate professionals. Its portfolio supports the effective management of intricate information and compliance needs across various sectors.

Revenue Streams: The company’s revenue primarily comes from legal professionals, contributing approximately USD 2.9 billion, followed by corporate clients at about USD 2 billion and tax and accounting services at roughly USD 1.4 billion. Additional contributions stem from Reuters News, generating approximately USD 869 million, and Global Print, which contributes around USD 486 million, adjusted for minor eliminations.

Market Capitalization: CAD 55.3 billion.

Strategic Importance: Thomson Reuters shines in the legal services stock landscape, especially with its legal research platform and AI-driven workflow tools, which are increasingly relevant given the rise in immigration bond hearings and related litigation. The company benefits from robust recurring revenues, impressive net profit margins of 20%, and a history of dividend growth coupled with proactive share buybacks. That said, investors should remain vigilant regarding declining earnings, margin pressures, fluctuating dividend policies, and intensified competition from AI-centric legal technologies. The discrepancy between analysts’ price targets and the current stock price could prove critical for potential investors evaluating Thomson Reuters.

Thomson Reuters presents a compelling case for investors, characterized by stable recurring revenue alongside share buybacks. However, the growing competition in legal AI may lead to tensions within this otherwise positive narrative.

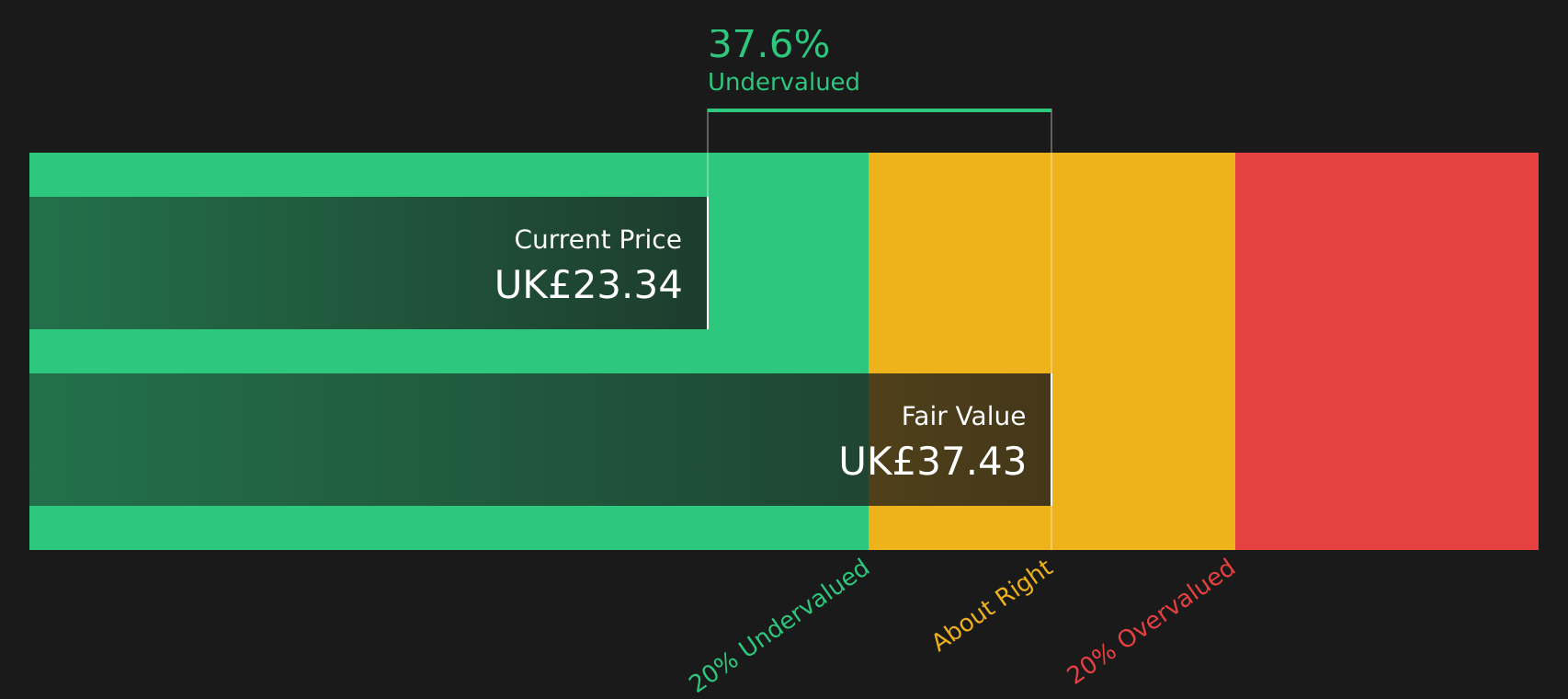

RELX

Company Overview: RELX is a UK-based information and analytics group, renowned for its platforms like LexisNexis, which provide data, research tools, and software to assist professionals across legal, risk, scientific, and event sectors in effective decision-making and compliance management.

Financial Composition: The bulk of RELX’s revenue comes from its risk division, contributing approximately £3.5 billion, followed by the science, technology, and medical sectors at about £2.7 billion. Additional revenue streams include the legal division (£1.8 billion), exhibitions (£1.2 billion), and print-related activities (£399 million).

Market Capitalization: £41.1 billion.

Strategic Position: RELX stands out for its robust data assets and a strategic push towards AI-driven products, notably through LexisNexis. This initiative aligns well with increasing U.S. bond hearing demands, suggesting heightened interest in immigration case management solutions. While the company enjoys stable earnings growth and solid profit margins of 21.5%, its pricing-to-earnings ratio remains elevated when compared to its UK professional services counterparts. Additionally, the company’s high debt levels inflate its return on equity (ROE). With a dividend yield of 2.89% and substantial share buybacks, RELX represents a fusion of quality and leverage risk that potential investors may find appealing.

RELX’s strong performance metrics and commitment to AI innovation suggest market confidence, although the underpinning leverage merits careful consideration by investors assessing broader sentiment.

These three companies are a mere starting point out of a larger landscape. A comprehensive analysis of the legal services sector reveals an additional 36 companies that present intriguing opportunities within immigration, litigation, and courtroom discussions. Utilizing analytical platforms can help you identify the most compelling narratives and trends relevant to your investment strategy.

Taking Control of Your Investment Strategy

If you view Robert Half or any of these companies as promising investment opportunities, consider using analytical tools to track their stock performance relative to fair valuation. This approach can help identify optimal entry points for your portfolio. Furthermore, managing your portfolio efficiently can filter out unnecessary noise, providing you with crucial updates. Investors can gain insights from a diverse community, exploring the most effective strategies and potential risks that could shape the market landscape.

Exploring Alternatives Beyond Legal Services

While currently under broad market radar, alternative investment opportunities are gaining momentum. Act proactively to explore dividend yields and AI infrastructure stocks, or investigate sectors poised for growth ahead of mainstream visibility.

This commentary is for informational purposes only. We employ objective methodologies based on historical performance and analyst forecasts. This analysis does not serve as financial advice or recommendations for specific stocks, nor does it consider individual financial situations. Our focus is on long-term evaluations based on fundamental data, but may not account for recent announcements or qualitative developments. Simply Wall St does not hold positions in any stocks discussed.

Investing Insights Simplified

Discover whether Thomson Reuters is undervalued or overvalued through our detailed analysis, encompassing fair value estimates, potential risks, dividends, insider transactions, and overall financial health.

Access free analysis

We welcome your feedback on this article. If you have any inquiries regarding its content, please contact us directly.